We believe there are several factors with the potential to favorably impact capital flows toward gold in 2017 and signal gold prices have resumed a major uptrend, such as:

- Gold stands to gain from safe haven flows from Europeans looking to hedge further upheaval as the coming year poses heightened political risk as Europe holds key elections in the Netherlands, France, and Germany. The populist movement brought about by immigration and uneven wealth distribution raises the prospect of the disintegration of the European Union and the euro currency.

- Gold historically is negatively correlated to financial assets. With equity market indexes at historic highs and bond prices skewed by central bank purchases, the prospect of financial assets correcting down as central banks attempt to back away from market intervention in favor of fiscal stimulus is quite high.

- President Trump’s economic agenda is expected to increase inflationary expectations as increased spending on infrastructure and penalizing foreign manufacturing leads to higher prices and upward pressure on wages in a tight labor market. While the Federal Reserve and other central banks have moved to foster inflation to lessen the burden of high sovereign debt levels and future entitlement obligations through aggressive monetary policy, it is questionable whether the Fed will be able to tame the inflation genie once it is out of the bottle due to the systemic risks posed by significantly higher interest rates on the value of interest sensitive instruments to its member banks. If the Fed is perceived to be behind the curve as it was in the 1970s, we believe gold will attract significant capital flows looking to protect purchasing power and hedge fixed income portfolios

- President Trump’s “Art of the Deal” tactic of starting off negotiations at ridiculous extremes to achieve favorable outcomes increases the risk of contentious trade negotiations and geopolitical tension risk with China and other trade partners.

- The likelihood of Trump failing to deliver on his economic promises and disappointing the markets in his first two years is certainly not out of the question. Trump’s policies have drawn comparisons to Ronald Reagan’s term in office with a high degree of optimism on Wall Street for similar economic growth. It should be noted, Reagan found the first two years of his presidency tough sledding with the stock market down 25%. Trump has the challenge of taking office with debt to GDP levels three times that of when Reagan took office along with interest rates at historic lows versus the Reagan era when rates were at historically high levels. Raising the possibility, the bulk of Trump’s fiscal stimulus plans may be crowded out as increased interest costs on the $20 trillion dollar U.S. debt in a rising interest rate environment kick in along with the $120 billion per year increase in baby boomer entitlements taking effect. The alternative is a growing budget deficit and continuing the trend of the past two administrations of doubling the total outstanding government debt every eight years.

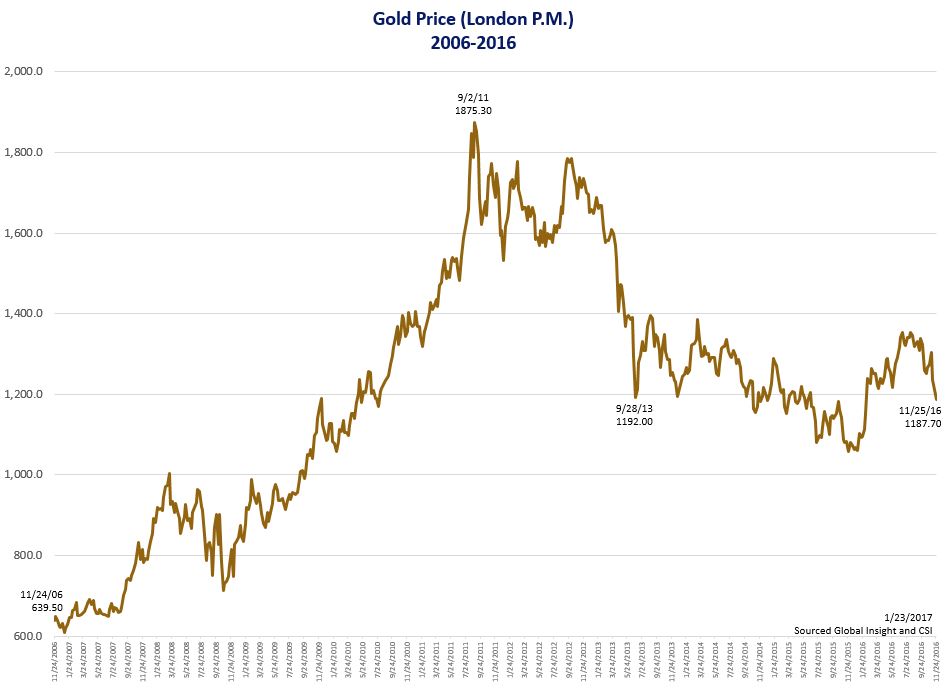

- Over the past decade, China has absorbed vast quantities of physical gold previously held in western vaults, mostly in London. Chinese gold consumption is unlikely to be traded back into the market for a quick trade as it tends to be held for strategic purposes versus the pervasive Western mentality of holding gold for a trade. The uptick in gold prices in the first half of 2016 to meet Western demand for physical by gold ETFs exhibited a level of tightness and sensitivity the gold market had not seen for a long time. The largest ETF, SPDR Gold Trust1, needed to borrow 26 tons of gold from the Bank of England to meet its backing requirement as inflows surged. The lack of physical gold available to satisfy settlement without borrowing in the London market illustrates that Western buyers will need to significantly bid up the price of gold in order to pry it back from Asia. This is a positive development as the reach for true price discovery of physical gold versus the massive paper gold market that settles its trades almost entirely through cash settlement gets closer to reality. In our opinion, the creation of gold out of thin air strictly off balance sheet wherewithal has negatively distorted gold prices and profitability of gold mining companies by making the supply of gold appear much greater than it truly is by over 100 times.

- A major development that may have a significant impact on increased physical gold demand is a new Shari’ah Standard for Gold instituted by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) in December 2016. The new Standard provides a definitive guidance on allowable gold products, potentially allowing 25% of the world’s population to invest in gold where it hadn’t been allowed in the past.

- Diverging monetary policy between the U.S. and other parts of the world poses several potential problems. The most troublesome is default risk increases for foreign borrowers of U.S. dollars as euro dollar availability is squeezed as U.S. interest rates move higher. Dollar denominated debt outside the U.S. is estimated at $14 trillion owed by both private corporations and sovereign governments.

Commentary

In our opinion, the heightened level of political and geopolitical uncertainty associated with the populist movement in Europe and the United States, combined with the systemic financial risk from eight years of radical monetary policy, has created an environment of unparalleled risk. Trump may prove successful in stimulating the necessary economic growth to service the increased debt burden placed on the economy over the past two administrations, but it seems prudent, in our opinion, to hedge with exposure to gold and precious metal equities against an unwinding process that may prove to be detrimental to the value of financial assets. We believe, markets may move ahead of Trump’s fiscal stimulus plan and the Federal Reserve by collapsing the bubble in the bond market in anticipation of rising inflation and ballooning budget deficits and foreign central banks’ need to sell U.S. treasuries to meet dollar obligations. A rapid spike in interest rates from current levels could trigger a cascading sequence of defaults that may lead to deflationary consequences if not handled swiftly and appropriately by policy-makers. In our opinion, if this were to occur a new monetary order in the context of a Bretton Woods Agreement2 could be enacted to instill confidence in the financial system, stabilize exchange rates and cap interest rates. Of note, Trump has surrounded himself with several advisers that are sound money advocates, such as Judy Shelton and Vice President Mike Pence. Therefore, it is not too farfetched to imagine a new Bretton Woods with gold having a role, perhaps as a reference point.

The SPDR Gold Shares ETF1 (NYSEARCA: GLD) tracks the price of gold bullion in the over-the-counter (OTC) market.

The Bretton Woods Agreement2, which was introduced in the late 1940s, after World War II, established a fixed exchange rate system, having been agreed upon at the Bretton Woods conference by the more than 40 countries that participated. The system was developed to give structure to international monetary exchanges and policies and to maintain stability in all international finance transactions and interactions.

{kind=link}