Market Commentary

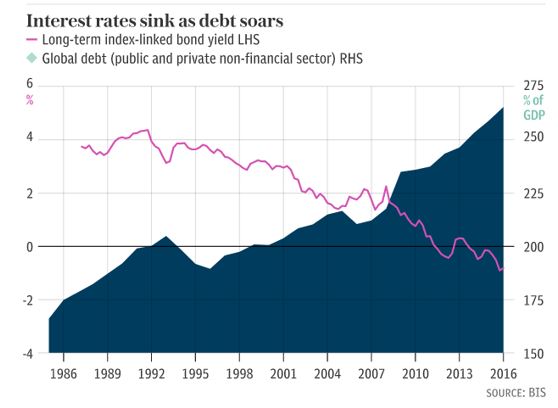

Since the Federal Reserve began the current rate hike cycle in December of 2015, gold prices have trended higher similar to the previous rate hike cycle in 2004 to 2007. With U.S. equity markets hitting new highs and the U.S. economy experiencing economic expansion for the longest period since WWII, there is a pretense in the market that the Federal Reserve’s radical monetary measures following the 2008 financial crisis have successfully navigated the global economy to port. Yet, the issues of too much debt and leverage that caused the last crisis have only been exacerbated over the past ten years of zero interest rates and central bank balance sheet expansion. According to the Institute for International Finance1, global debt at the end of 2016 stood at $217 trillion, up 47% in ten years, and global debt to Gross Domestic Product (GDP)2 stands at a staggering 325%. Policy makers have merely papered over the structural problems in the economy, basically kicking the proverbial can down the road until the next crisis hits. The irony is Federal Reserve Chairwoman, Janet Yellen, recently commented that she didn’t think another financial crisis would take place “in our lifetimes;”3 a statement historians will no doubt mark as the top of central bank hubris.

Meanwhile, the Bank for International Settlements (“BIS”)4 disagrees with Janet Yellen. In its recent annual report, the BIS believes the ills from the Lehman crisis in 2008 have not been rooted out of the system and that the global economy is stuck in a permanent trap of financial boom-bust cycles. With the Federal Reserve pushing interest rates higher and intent on shrinking its balance sheet, the BIS believes the financial system is about to be tested. The BIS’s chief economist, Claudio Borio, doesn’t believe it will end well. He stated, “The end may come to resemble more closely a financial boom gone wrong, just as the latest recession showed, with a vengeance.”5

The top of modern financial boom-bust cycles is characterized by not only historically elevated asset prices but also investor complacency by market participants, as is currently evident by persistently record low readings in the volatility index (“VIX”).6 The trigger for investors to run to the exits is elusive to gauge, but in our view, what is not difficult to foretell is that a potential VIX mean reverting event may come with a heightened level of ferocity that has not been seen to date. In our opinion, the explosion of passive investing through exchange-traded funds (“ETFs”)7 and computer algorithmic trading over the past ten years has set the stage for a massive mismatch of liquidity in the market between the underlying index components versus the ETFs at the point a collective sell signal has been triggered, which is a risk that has yet to become fully understood by the market. We believe gold’s monetary attributes positions gold assets to gain disproportionately as investors seek a safe haven to preserve purchasing power in such an environment.

Source: BofA Merrill Lynch Global Investment Strategy, Global Financial Data, Bloomberg, USDA, Savills, Shiller, ONS, Spaenjers, Historic Auto Group. Note: Real Assets (Commodities, Real Estate, Collectibles) vs. Financial Assets (Large Cap Stocks, Long-term Govt Bonds)

Gold Mining Industry

We are of the belief the supply of newly mined gold is set to shrink materially over the next decade even in the face of significantly higher gold prices. There are two main factors impacting mine supply: the first is the long lead time from discovery to production of seven to 20 years; the second is the lack of new deposits in stable jurisdictions with acceptable after-tax rates of return despite the high level of exploration expenditures over the past decade (punctuating the scarcity value of gold). The challenge for the industry’s largest producers is to replace depleting reserves and production without destroying shareholder value through ill-conceived mergers and acquisitions. Consequently, we have seen the major gold producers sell off mines with limited reserve lives and focus on a smaller production platform that each believe is reasonably sustainable with higher margins. The result is less production for the sake of option value production going forward.

Your Fund’s investment strategy remains a disciplined approach to searching out value and growth opportunities across all segments of the gold and silver mining industry on a global basis. We believe companies that possess strong management, large reserves in the ground in stable jurisdictions, and exhibit capital discipline while holding equity dear may be the companies that outperform over time. Your Fund has the flexibility to maneuver within the precious metals sector to invest in opportunities that larger funds and exchange traded funds cannot; from major gold producers with over one million ounces of annual production to junior producers with less than 100,000 ounces of annual production to small exploration and development companies with micro capitalizations.

Conclusion

The unlimited printing press capability of central banks has created an unhealthy level of arrogance on the part of monetary policy makers that they can now deal with any financial crisis simply by using a monetary bazooka. Former Federal Reserve Chairman, Ben Bernanke, once remarked that the Fed had the printing press and could drop money figuratively from helicopters to fight deflation. Prompting Jim Grant of Grant’s Interest Rate Observer to remark regarding the dollar, “If it is so easily reproduced, what is it worth?” European Central Bank (“ECB”)8 head, Mario Draghi, notably made the statement that the ECB “will do whatever it takes” to save the euro. What central banks and the academics that populate the institutions may very well learn is that market forces have a history of exposing the abuse of the printing press. With global private and public debt levels at record highs and financial assets valuations elevated, the monetary tightening path the Fed has embarked on may soon set off a domino event that tests the credibility of monetary policy makers intent on debasing currency for the sake of socializing risk. Consequently, we believe the rationale for owning gold assets as protection against monetary policy decisions designed to promote currency debasement remains a sound investment strategy. The current environment of disinterest by most investors toward gold mining equities creates an opportunistic entry point for investors looking to establish gold exposure or rebalance their portfolios.

Gregory M. Orrell

Portfolio Manager

July 21, 2017

5549-NLD-07/26/2017 (Shareholder Letter)

The Institute of International Finance1 is the global association of the financial industry, with close to 500 members from 70 countries.

Gross domestic product (GDP)2 is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

3Cox, J. (2017, June 27). Yellen: Banks’ very much stronger’; another financial crisis not likely ‘in our lifetime’ retrieved from CNBC.com on July 21, 2017.

Bank for International Settlements (BIS)4 is an international financial organisation owned by 60 member central banks, representing countries from around the world that together make up about 95% of world GDP.

5Mortimer, C. (2017, June 25). Great recession fears as bankers warn next global crash could arrive ‘with a vengeance’, warns BIS retrieved from telegraph.co.uk on July 21, 2017.

Volatility Index6, which shows the market’s expectation of 30-day volatility. It is constructed using the implied volatilities of a wide range of S&P 500 index options.

Investors cannot invest directly in an index.

An ETF7, or exchange-traded fund, is a marketable security that tracks an index, a commodity, bonds, or a basket of assets like an index fund.

The ECB8 is the central bank responsible for the monetary system of the European Union (EU) and the euro currency.

For more information or to schedule a call with Greg Orrell, Portfolio Manager, please call 1-800-779-4681.

Investors should carefully consider the investment objectives, risks, charges and expenses of the OCM Gold Fund. This and other important information about a Fund is contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing. Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors are not affiliated.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}