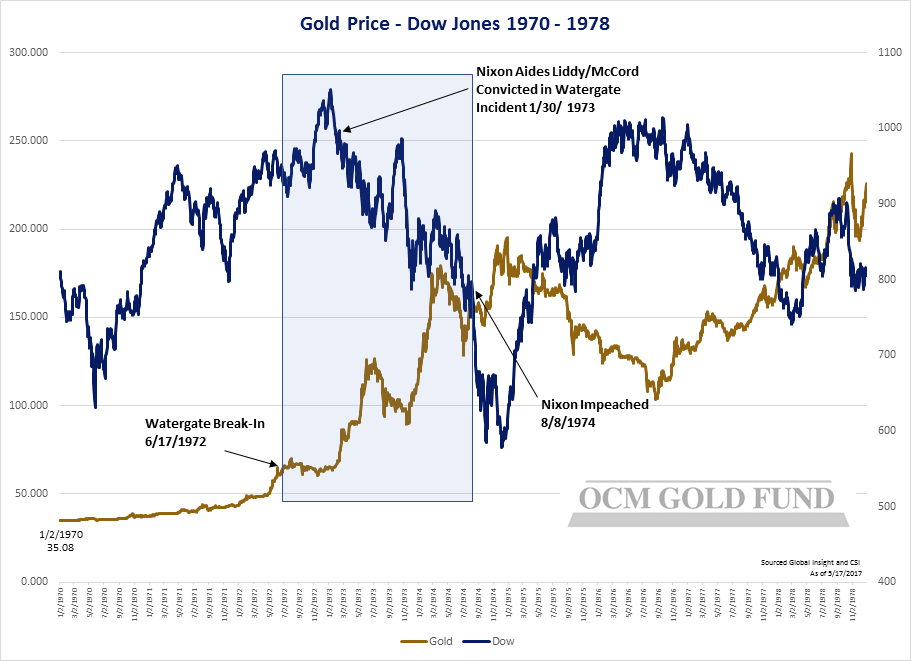

Trump – Headline Risk and DC Uncertainty Unlikely to Diminish

President Trump’s enemies in the Washington DC political establishment appear intent on finding a way to remove him from office. If Trump’s foes successfully bring impeachment proceedings, a review of the Watergate Nixon impeachment timeline’s impact on equities and gold might be helpful. From the date of the Watergate break-in arrests on 6/17/1972 to Nixon’s impeachment on 8/8/1974, the gold price rose 154% and the Dow1 declined 21% (The Dow continued to decline until 12/7/1974 when it bottomed down 39% from the break-in date).

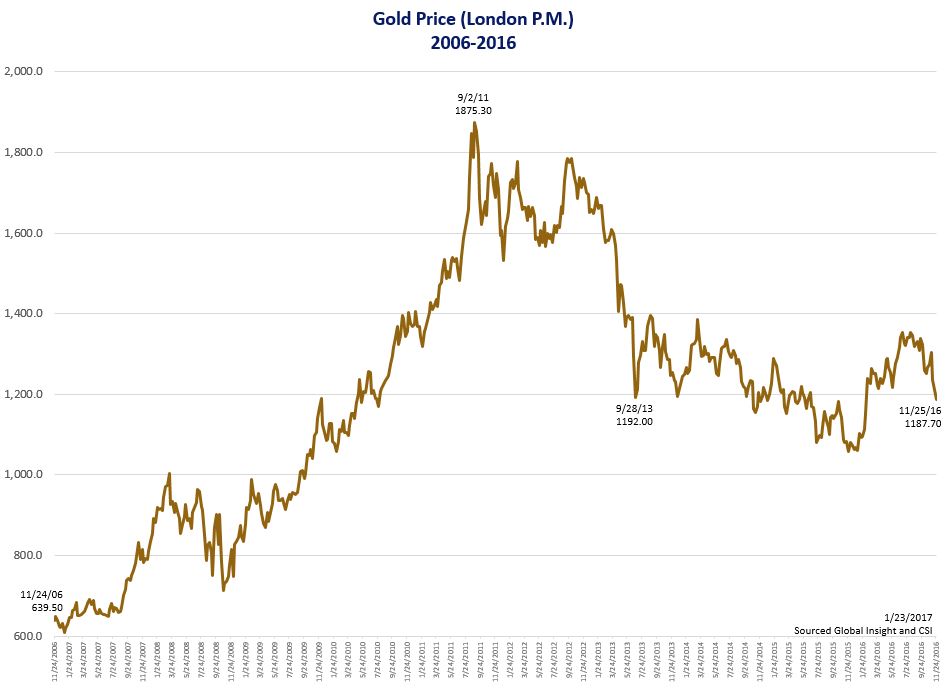

Chart Sourced: Global Insight and CSI

Gold priced sourced from London Gold PM Fix.

Past performance does not guarantee future results.

You cannot invest directly in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. The referenced indices are shown for general market comparisons and are not meant to represent the Fund.

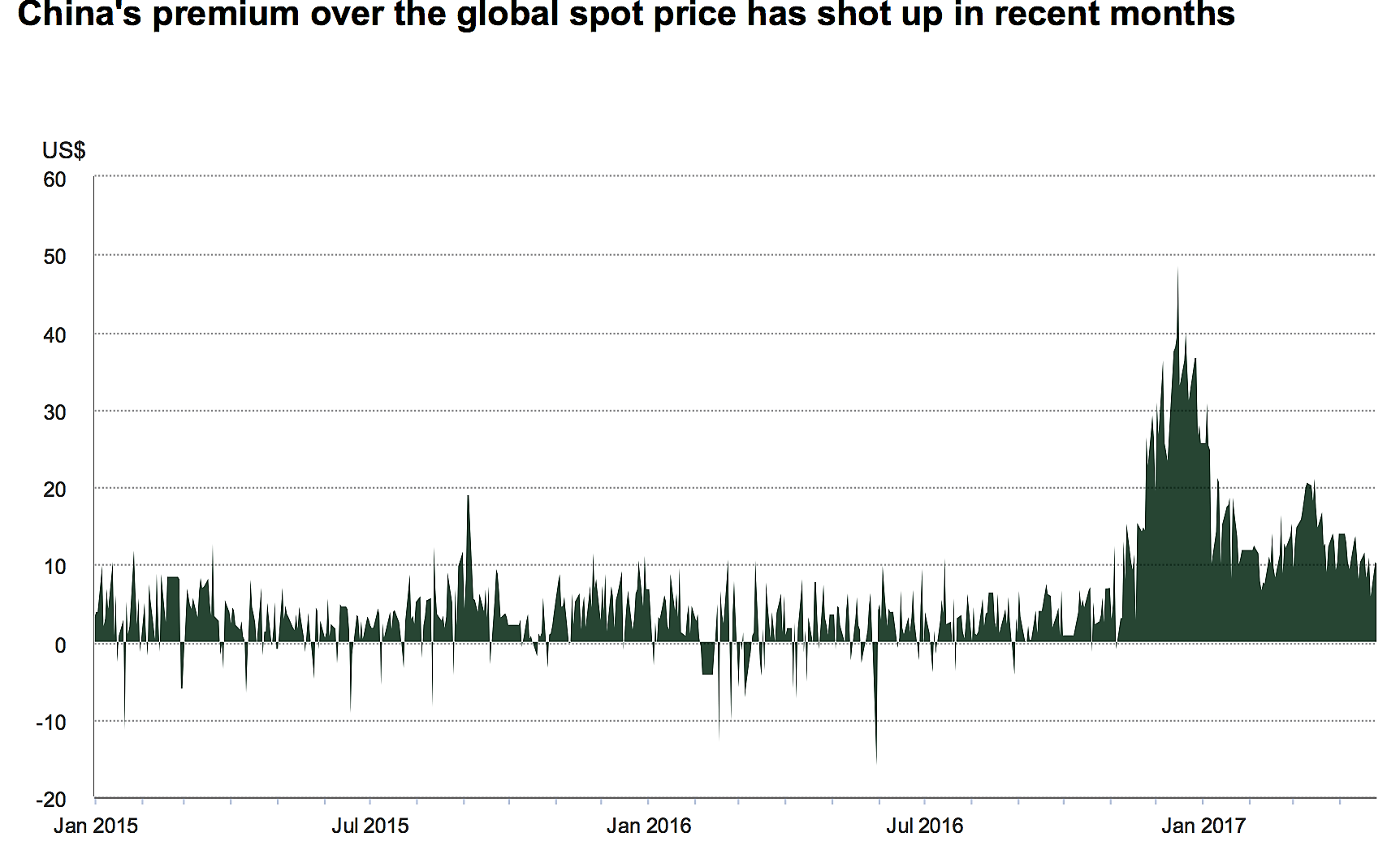

China’s Gold Premiums

The increase in gold premiums in China over spot gold prices in recent months may indicate Chinese investor anxiety over the election of Donald Trump or coincidently growing nervousness within China over the fragility of its financial system that is being tested with failures in the shadow banking sector. The bottom line is Chinese demand is strong and, according to Shanghai Gold Exchange (SGE)2 statistics through the first four months of 2017, Chinese gold demand is matching the record setting pace of 2013 when China drained gold from bullion vaults in London.

Chart Source: Goldcore

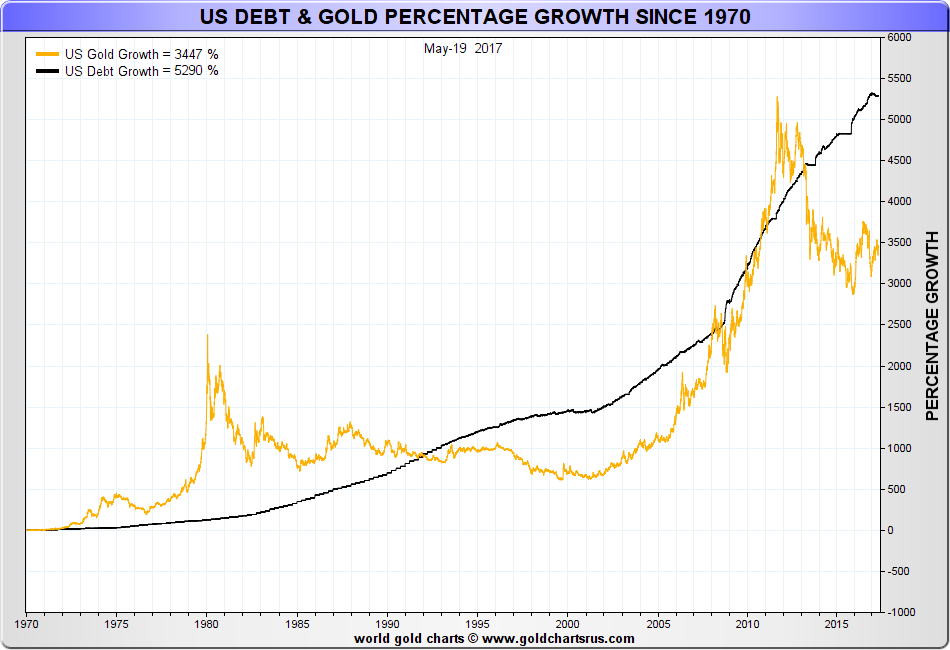

Gold and US Debt

Since 1970 there is a corresponding relationship between the growth in US debt obligations and the gold price. The long-term case for owning gold assets is illustrated by this chart as the gold price gravitates toward the rate of growth line of US debt like a magnet. Unless one believes US debt levels have peaked, despite debt interest servicing costs at historic lows, gold prices appear set to move higher over time. Moreover, rising interest rates have the potential to exponentially drive US debt levels higher reinforcing the view that rising rates and rising gold prices will be reflective of a US economy unable to service existing debt levels without debt monetization and massive monetary debasement.

Chart Sourced: GoldCharwtsRUs.com

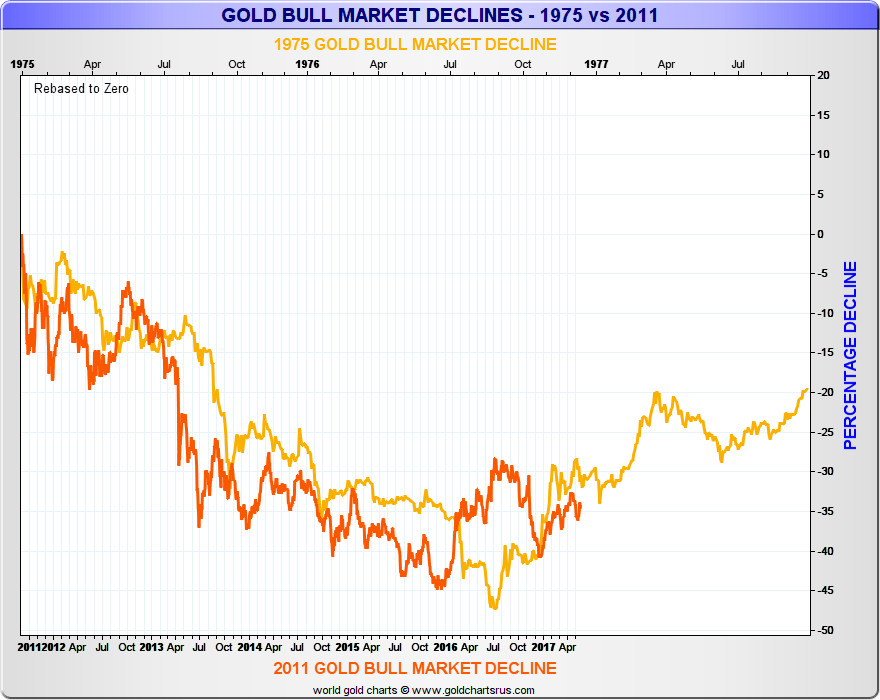

Gold Price Still Tracking 70’s Bull Market Correction from 1975-76

From the 2011 peak of $1900, gold prices are closely tracking the 1975-1976 percentage decline in gold that saw gold prices drop from $190 to $103 prior to peaking at $850 four years later. Another zero has been added to the gold price equation over the last 35 to 40 years of monetary debasement. Forecasts for gold prices to reach $3,500 to $4,500 range are not that outlandish, in our opinion. Basically, equal to when gold prices were $35 then $350/oz3.

Chart Sourced: GoldChartsRUs.com

Gold Mining Share Volatility – Tail Wagging the Dog – JNUG/GDXJ

As of May 23rd, $2.6 billion or 67% of Van Eck’s Junior Gold Mining Exchange Traded Fund ETF (GDXJ)4 total assets of $3.9 billion were directly tied to JNUG – Direxion’s 3X levered ETF5 to the GDXJ. Over the first half of the year, JNUG has accounted for in/out flows of over $2 billion into GDXJ forcing Van Eck to broaden its basket of “junior” miners to include intermediate and a couple of senior mining companies which it expects to announce on June 7th. Meanwhile, the market is anticipating the rebalance by selling down junior miners held in the GDXJ. Since the methodology announcement by Van Eck on April 12th the GDXJ is down 16.9% versus Gold price down 1.8 % and the HUI6 down 9.0%6. Derivatives on top of derivatives may have gotten out of hand, ya think?

1 The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq.

2 Shanghai Gold Exchange (SGE) is a non-profit self-regulatory organization, approved by the State Council, organized by the People’s Bank of China, and registered with the State Administration for Industry & Commerce, for the purpose of trading gold, silver, platinum and other precious metals.

3 Comex Close Price

4 The Market Vectors Junior Gold Miners EFT (GDXJ) attempts to replicate the price and yield performance of the Market Vectors Junior Gold Miners Index.

5 The Direxion Daily Junior Gold Miners Index Bull and Bear 3X Shares (JNUG) seek daily investment results, before fees and expenses, of 300% or 300% of the inverse (or opposite) of the performance of the MVIS Global Junior Miners Index. There is no guarantee these funds will meet their stated investment objectives.

6 Sourced from www.nasdaq.com. Gold prices sourced from London PM gold Fix. The NYSE Arca Gold BUGS Index is a modified equal dollar weighted index of companies involved in gold mining. BUGS stands for Basket of Unhedged Gold Stocks. It is also referred to by its ticker symbol “HUI”.

For more information or to schedule a call with Greg Orrell, Portfolio Manager, please call 1-800-779-4681.

Investors should carefully consider the investment objectives, risks, charges and expenses of the OCM Gold Fund. This and other important information about a Fund is contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing. Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors are not affiliated.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

Investments cannot be made in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Past performance is no guarantee of future results.

{kind=link}