“It is Time!”

A major cyclical turn is at hand, in our opinion, as the Federal Reserve’s rate hike cycle appears to be hitting the wall with global economic growth decelerating and equity markets and consumer confidence rolling over from cycle peaks. Gold has historically been the reciprocal of financial assets as capital gravitates toward gold assets in periods of economic uncertainty for safety of purchasing power and away from gold assets in periods of economic growth and rising consumer confidence.

While we believe December 2015 marked the bottom of the bear market for shares of gold mining companies as the Federal Reserve began its long-telegraphed rate hike cycle, it is our opinion, 2018 may likely prove to be the bottom in sentiment toward shares of gold mining companies. The washout in sentiment toward gold assets was highlighted by Vanguard changing the mandate for its precious metals and mining fund to a contra cyclical fund in July of 2018. Interestingly, Vanguard rang the bell for the peak in the Nasdaq1 and the low in gold share sentiment in 2000 when it changed the mandate of its gold fund to include base metal equities.

The list of factors and antidotal evidence pointing to a significant shift in sentiment toward gold assets may be on the horizon includes the following, in our opinion:

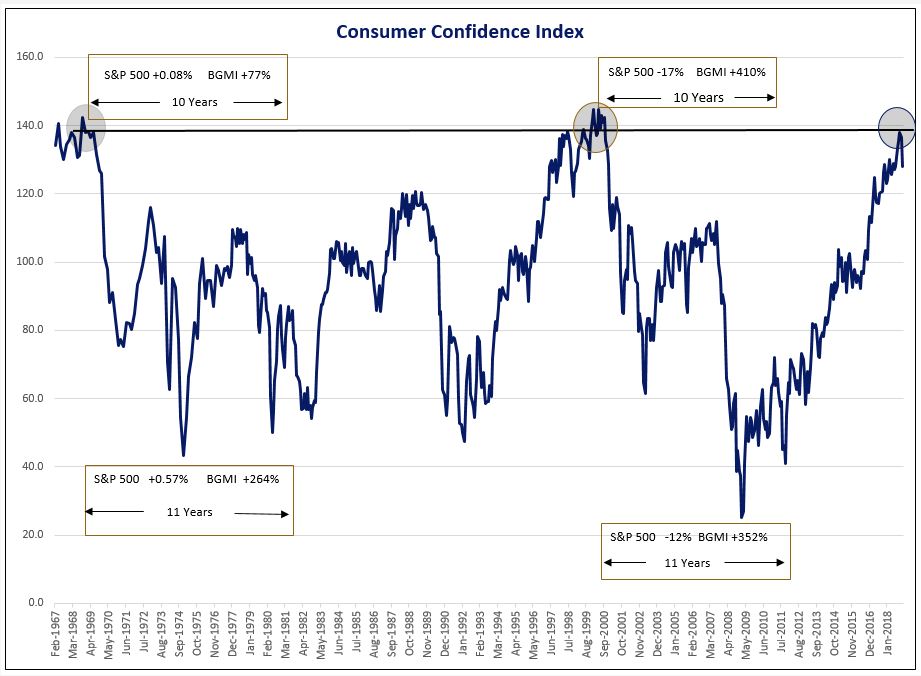

- The two prior times the Conference Board’s Consumer Confidence Index2 declined from the level reached in October 2018 (April 1969 and September 2000), shares of gold mining companies significantly outperformed the S&P 5003 over the following ten- and eleven-year periods (see chart).

- Despite the second longest U.S. economic expansion, total Federal debt outstanding is accelerating as tax reform and rising interest expense propel the U.S. budget deficit upward and total Federal debt outstanding to $22 trillion. Gold prices are highly correlated over time to total Federal debt outstanding with a 90% correlation since Nixon closed the gold window in 1971 and 87% since 2000.

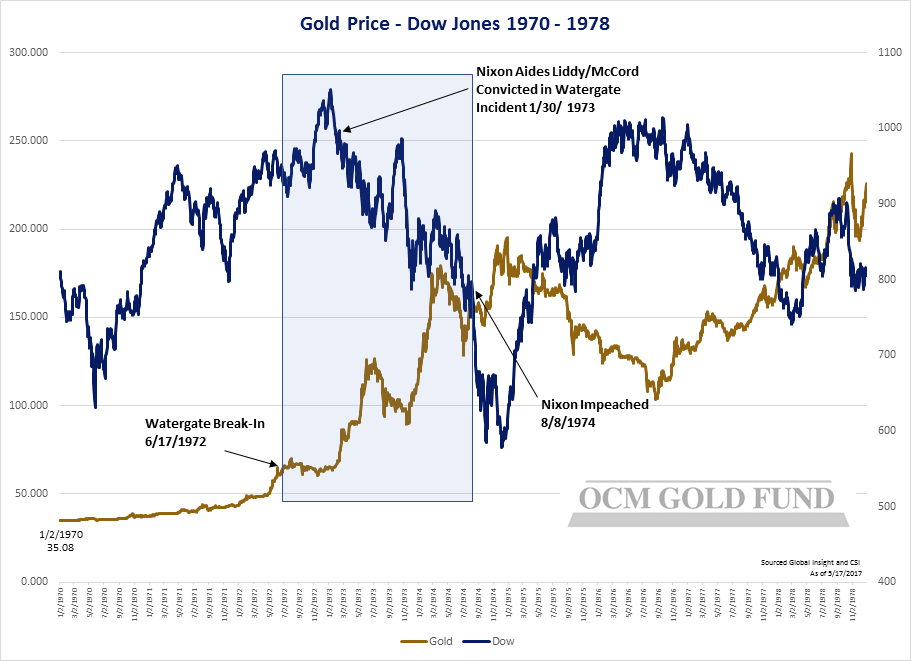

- Democratic party retaking the House of Representatives in November 2018 elections has increased the acrimonious political atmosphere in Washington, raising the odds of Trump impeachment proceedings gaining momentum in 2019. Further, as the 2020 presidential election grows closer, markets may fear a democratic victory by a far-left leaning candidate that promises taxing the “rich” to redistribute wealth and undoing Trump’s move to relax the government regulatory environment.

- The Fed’s current rate hike cycle at 36-months is the 2nd longest to the 39-month hike cycle from 1977 to 1980. It stands to reason with global debt levels up 60% since 2008, attempts to “normalize” rates would materially impact global liquidity and growth at much lower rate levels than previous economic cycles and lower than what the Federal Reserve may have hoped for. The prospect for the Fed to pause its rate hike cycle and eventually lower interest rates over the next two years will, in our opinion, be viewed negatively for the U.S. dollar and positively for U.S. dollar gold price.

- Gold bull markets are characterized by gold prices rising versus all currencies. In 2018, gold was at or near all-time highs in 72 currencies which has historically been a precursor for gold prices to rise versus the U.S. dollar.

- Record sovereign debt levels both in nominal terms and debt to Gross Domestic Product4 levels encourages currency debasement going forward to inflate debt repayments away.

- Central bank gold purchases by Russia, China, Turkey, India, Poland, Hungary and Kazakhstan, not only reinforce gold’s monetary status, but further raise speculation a currency bloc based on gold to rival the U.S. dollar may be in the works. Both Chinese and Russian officials have been quoted as believing the U.S and U.S. dollar are vulnerable due to its extended debt position.

- A sharp sell-off in the fourth quarter led to a 4% decline for the S&P 500 for all of 2018. With global economic activity slowing, earnings estimates for the S&P 500 are beginning to be revised down. Despite equity valuations being stretched by most valuation metrics, such as total market capitalization to GDP, the prospect of a bear market remains a distant thought for most investors and strategists on Wall Street. If the broad equity market continues down in 2019, investors may start to become disillusioned and search for returns elsewhere. In such a scenario, it is our opinion, gold assets will attract capital as they did in the 70’s and 2000’s.

- The current economic expansion fueled by the extreme monetary policies of central banks and more recently by Trump tax reforms and deregulation is considered in the eighth or ninth inning. The onset of a recession has historically driven gold prices 20% higher as the Federal Reserve moves to an accommodating monetary policy.

- Trade wars, social tensions, full employment and high government debt levels are ingredients for accelerated price inflation and currency debasement.

BGMI = Barron’s Gold Mining Index

Source: Sharelynx

Conclusion

Being able to recognize major market cycles is a key component in creating or preserving long-term wealth. Such a period is at hand with gold assets set to outperform most asset classes over the next ten to eleven years, in our opinion. With both consumer confidence at an extreme and equity valuations historically stretched, it is understandable sentiment toward gold assets is washed out and similar to the lows in 2000. As it becomes clear to the market that the weight of past fiscal and monetary policy decisions has left the Federal Reserve little choice but pursue a path that accelerates debasement of the U.S. dollar or risk a politically untenable deflationary meltdown, capital will flow toward gold assets seeking a safe port in a storm, in our opinion. Consequently, we believe the rationale for owning gold assets to mitigate risks against monetary policy decisions designed to promote currency debasement remains a sound investment strategy. The current environment of disinterest by most investors toward gold mining equities creates an opportunistic entry point for investors looking to establish gold exposure or rebalance their portfolios.

Nasdaq1 is a global electronic marketplace for buying and selling securities, as well as the benchmark index for U.S. technology stocks.

The Consumer Confidence Index (CCI)2 Survey is an index by The Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future. Investments cannot be made in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

S & P 5003 is a registered trademark of McGraw-Hill Co., Inc. is a market capitalization-weighted index of 500 widely held common stocks. You cannot invest directly in an index.

Gross domestic product (GDP)4 is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period.

For more information or to schedule a call with Greg Orrell, Portfolio Manager, please call

1-800-779-4681.

Investors should carefully consider the investment objectives, risks, charges and expenses of the OCM Gold Fund. This and other important information about a Fund is contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing. Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors are not affiliated.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

Past performance is no guarantee of future results.

6137-NLD-01/29/2019

{kind=link}

{kind=link}