Dutch Central Bank Reaffirms Gold’s Preeminent Monetary Characteristics

De Nederlandche Bank (DNB) recently updated its website regarding its gold holdings with the following statements that are worth noting. The phrases, “In times of financial crisis” or “If the system collapses,” were of particular interest considering the present uncertain state of global monetary policy. The information below is from the article titled “DNB’s Gold Stock.”

- “De Nederlandsche Bank holds more than 600 tonnes of gold. In our opinion, a bar of gold always retains its value, crisis or no crisis. This creates a sense of security. A central bank’s gold stock is therefore regarded as a symbol of solidity;

- Shares, bonds and other securities are not without risk, and prices can go down. But a bar of gold potentially retains its value, even in times of crisis. That is why central banks, including DNB, have traditionally held considerable amounts of gold. Gold is the perfect piggy bank it’s the anchor of trust for the financial system. If the system collapses, the gold stock can serve as a basis to build it up again. Gold bolsters confidence in the stability of the central bank’s balance sheet and creates a sense of security;

- In times of financial crisis, DNB’s physical gold stock functions as an ultimate reserve asset and as an anchor of trust. The gold stock serves to cover ultimate systemic risks.”

German Central Bank Adds to Gold Reserves for First Time in 31 Years

Although it was a relatively small amount of 90,000 ounces, International Monetary Fund (IMF)1 data shows the Bundesbank joined the growing number of central banks adding to its gold holdings for the first time in 31 years. Earlier in the year, fellow European Union members, Hungary and Poland, purchased gold for the first time in over 20 years. The increased participation in the gold market by central banks, in our opinion, is either a statement against the United States and the U.S. dollar or central banks positioning for some type of new monetary order that may be needed in a systemic collapse, per the DNB statement.

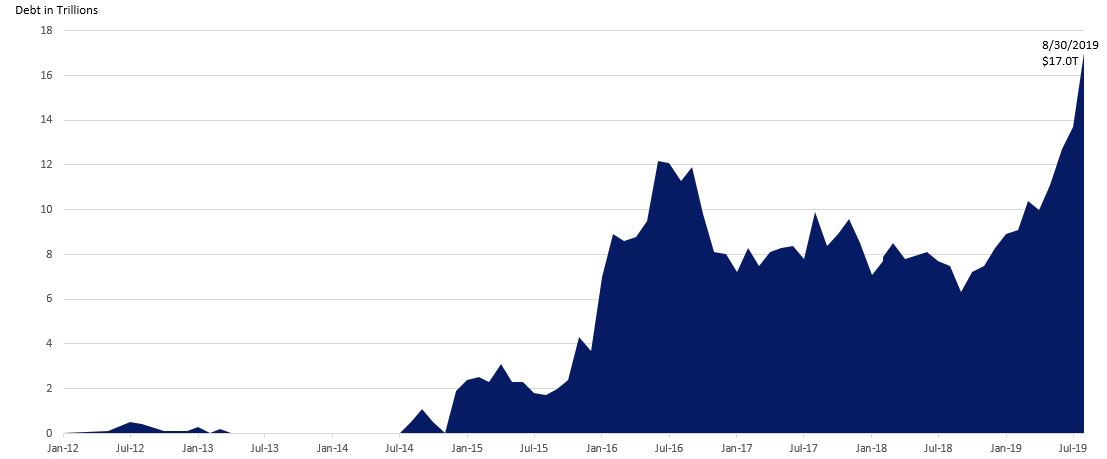

Insanity of Negative Yielding Debt Hits $17 Trillion

Negative yielding debt makes absolutely no rational economic sense – the price paid for a bond exceeds the amount received upon maturity, including interest. Who in their right mind pays for the right to have default risk? Further, if inflation is factored in, negative yielding debt is $36 trillion. Is there that much fear of deflation or is it just pure monetary madness?

Data As of 8/30/19 Source Bloomberg

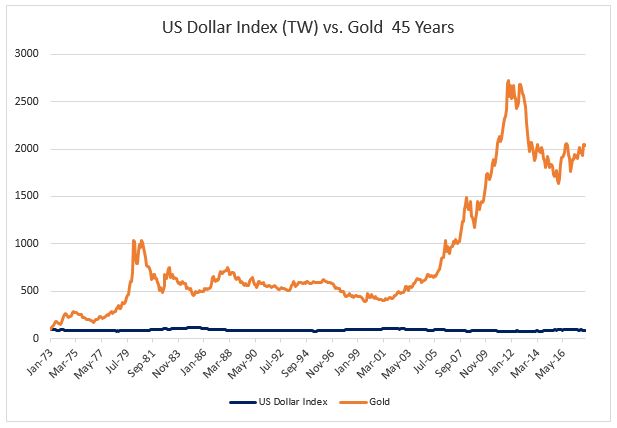

Long Term Gold Price Correlation to the US Dollar Index

The inverse relationship of gold and the U.S. Dollar Index2 is often cited by analysts attempting to understand gold price movements. One of the characteristics of a bull market in gold is that it rises against all currencies as countries engage in competitive devaluations, especially in times of economic contraction or during a recessionary period. This is best illustrated by the long-term chart of the Dollar Index and Gold Price3 over the past 45 years; basically, after President Nixon closed the gold window in 1971. By the way, over the past 12 months, gold is rising versus all currencies.

Source: Federal Reserve of Saint Louis

Past performance is no guarantee of future results. Investors cannot directly invest in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

2020 U.S. Political Uncertainty Bullish for Gold/Gold Assets?

We believe capital will be looking to hedge the uncertainty of the U.S. Presidential Election in 2020, if it has not already started. In our opinion, the prospect of Trump’s corporate tax cuts being unwound, along with a progressive democratic agenda, sets the stage for gold assets to be the assets of choice for diversifying perceived political risk.

See our latest Fund Fact Sheet.

International Monetary Fund (IMF)1 is an international organization that aims to promote global economic growth and financial stability, to encourage international trade, and to reduce poverty

The U.S. dollar index (USDX)2 is a measure of the value of the U.S. dollar relative to the value of a basket of currencies of the majority of the U.S.’s most significant trading partners. This index is similar to other trade-weighted indexes, which also use the exchange rates from the same major currencies.

For more information or to schedule a call with Greg Orrell, Portfolio Manager, please call 1-800-779-4681.

Investors should carefully consider the investment objectives, risks, charges and expenses of the OCM Gold Fund. This and other important information about a Fund is contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing. Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors are not affiliated.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

Investments cannot be made in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Past performance is no guarantee of future results.

{kind=link}

{kind=link}