Gold prices have rallied versus all currencies following the British referendum vote to leave (Brexit) the European Union (EU). We expect further increases in the gold price and gold mining shares as the market focuses on slower global economic growth, central bank easing, negative interest rates, declining credit quality, increased counter party risk and competitive currency devaluations. Here are a couple of brief thoughts:

- Brexit vote expected to trigger sustained inflows into the gold market as a period of protracted uncertainty surrounding the future of the EU destabilizes the euro as a reserve currency. SPDR Gold Trust (GLD) inflows the day following the vote amounted to 18.4 tonnes to 913 tonnes, the highest since July 18th, 2013.

- Federal Reserve interest rate increases and rhetoric are off the table for the foreseeable future.

- Negative interest rates have reached over $8 trillion of sovereign debt in Europe. Anticipation is negative rates will spread to bank deposits which should drive demand toward gold and holding physical cash as insurer Munich Re has already a bit in that direction.

- Decline in euro and pound offers cover for China to devalue yuan further leading to export of deflationary pressures putting further pressure on central banks to debase currencies on a competitive basis.

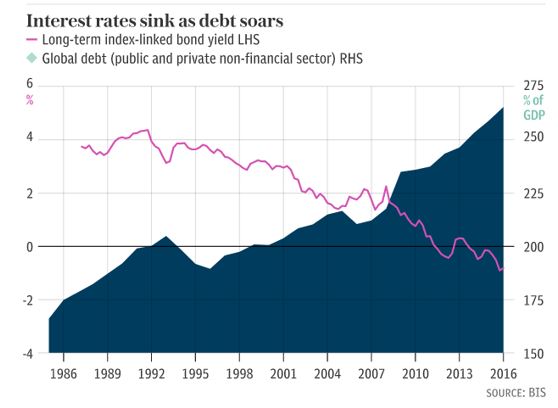

- The prospect of the global economy slipping into recession exposes credit quality issues for both corporates and sovereigns. Global debt has increased over 40% since 2008 financial crisis.

- Brexit outcome increase US political uncertainty leading up to Presidential election.

- Budget deficits likely to grow as calls for fiscal stimulus grow louder as monetary policy fails to stimulate economic growth outside of rising financial asset prices.

- Central bank “monitoring” of the gold market likely to curb initial gold price advance in order to manage negative market psychology as gold acts as an economic fever thermometer.

- Gold and gold assets are an under-owned asset class with the market cap of the entire gold mining industry approximately $180 billion versus JP Morgan’s market cap of $210 billion.

- Gold mining company reserves in the ground should gain appreciation as the market loses confidence in “paper gold” assets as the physical gold market tightens with increased investment flows and the ratio of gold futures contracts to warehouse inventories rises punctuates the scarcity of physical gold to the amount derivative gold instruments traded on a daily basis.

- Gold mining industry earnings set to show accelerated earnings growth versus the S&P 500* in a rising gold price environment setting the sector up to attract further investment flows.

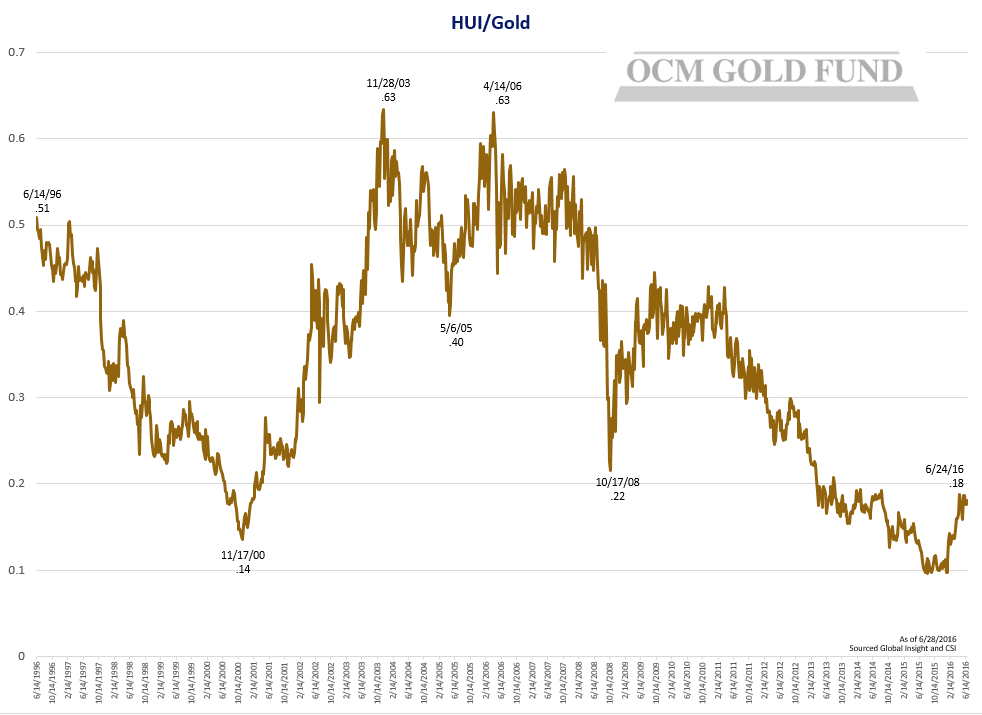

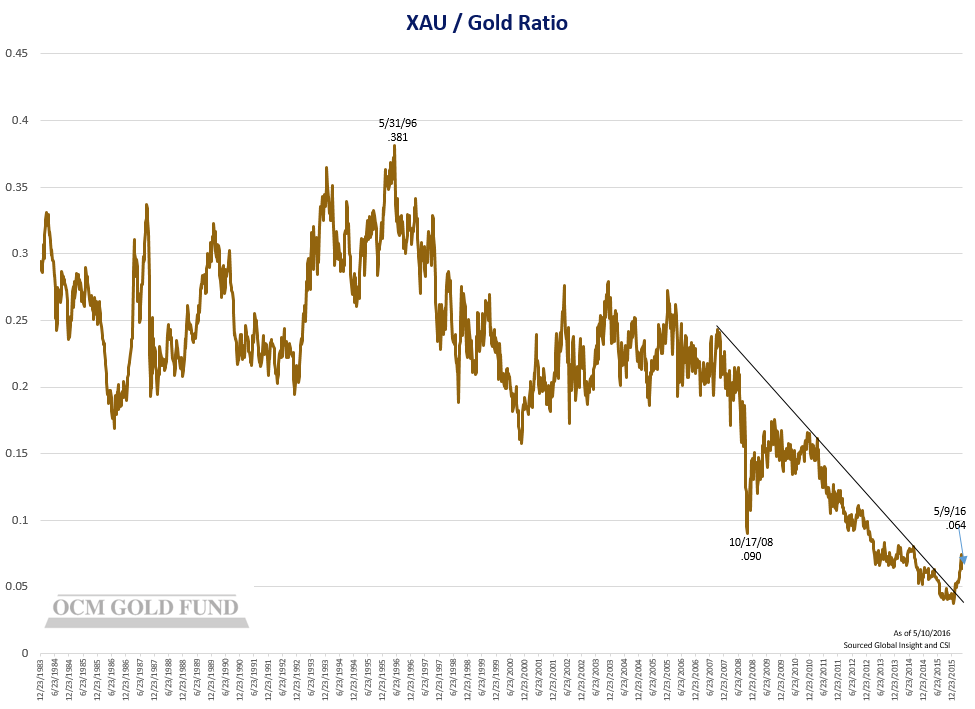

- Gold Mining share indexes versus gold remain in historically depressed levels with the HUI/Gold **ratio sitting not far off the level seen at the 2000 lows. (See chart)

Sourced Global Insight and CSI

* S & P 500

The S&P 500® Index is a registered trademark of the Standard & Poor’s Corporation and is an unmanaged broadly based index of the common stock prices of 500 large U.S. companies.

** HUI

The HUI, or gold BUGS index, is the AMEX’s index measuring gold companies that do not hedge their gold production beyond a year and a half.

Not a “Lehman Moment” – Yet

There is quite a bit of commentary that Brexit is not a “Lehman Moment” because it is a political event and not a credit event. While that is certainly true, the fallout can turn into a credit event as market turmoil leads to what former Fed Chairman Alan Greenspan once referred to as a “cascading sequence of defaults”. When the Archduke Franz Ferdinand of Austria was assassinated in 1914, it was not a credit event either, but it triggered a domino of events that led to credit markets going no bid at the time and the fall of the autocratic empires of Russia, Turkey and Austria-Hungary and ultimately World War I. Most credit events are a result of a separate event to begin with.

DUST and NUGT – Buyer Beware

Today’s market carries increased risk due to derivative trading instruments that trade based on other derivative instruments. We are repeatedly asked by financial advisors about Direxion’s 3X leveraged precious metals ETF products that track the gold market both up (NUGT) and down (DUST). First off, we are not big fans of leveraged ETF’s and the jury may still be out on ETF’s in general. That said, all you need to know about NUGT and DUST is that $10,000 invested in each vehicle upon inception on 12/8/2010 was worth the following on 6/24/2016.

NUGT – $57.55

DUST – $421.34

The Direxion Daily Gold Miners Bull 3x Shares (NUGT) is a 3x leveraged exchange-traded fund (ETF) that should be used for short-term trades only.

The Direxion Daily Gold Miners Bear 3x Shares (DUST) is a 3x leveraged exchange-traded fund (ETF) that should be used for short-term trades only.

In Gold We Trust

Lichenstein asset manager Incrementum AG released its extensive report on gold entitled “In Gold We Trust” on June 28th. The link is below and you are encouraged to take a look. It is good work.

http://www.lumopolis.org/In_Gold_we_Trust_2016-Extended_Version.pdf

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}