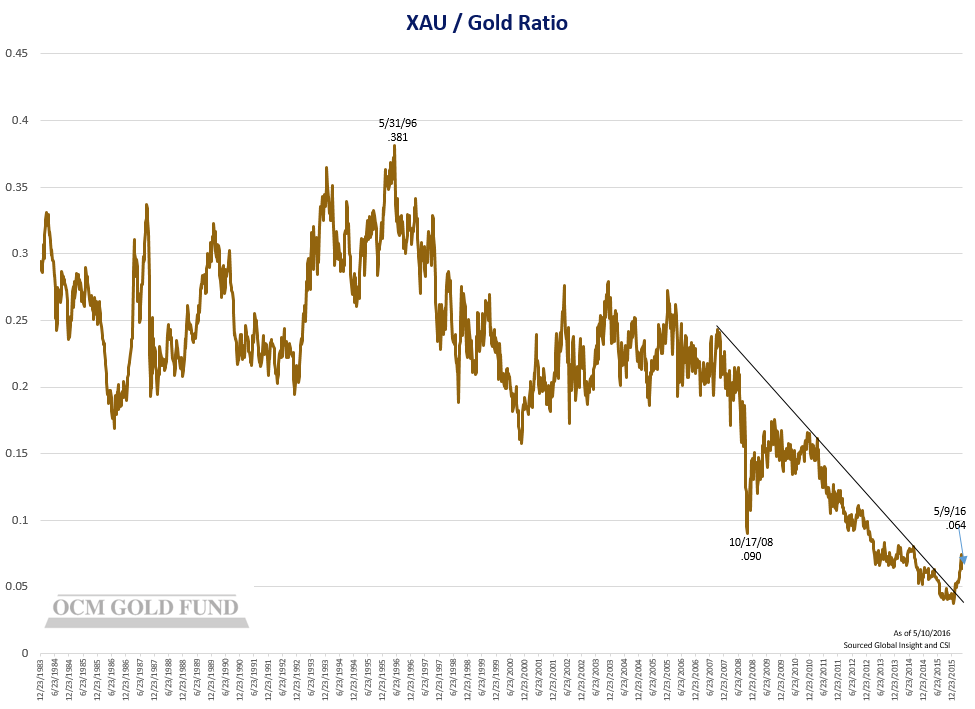

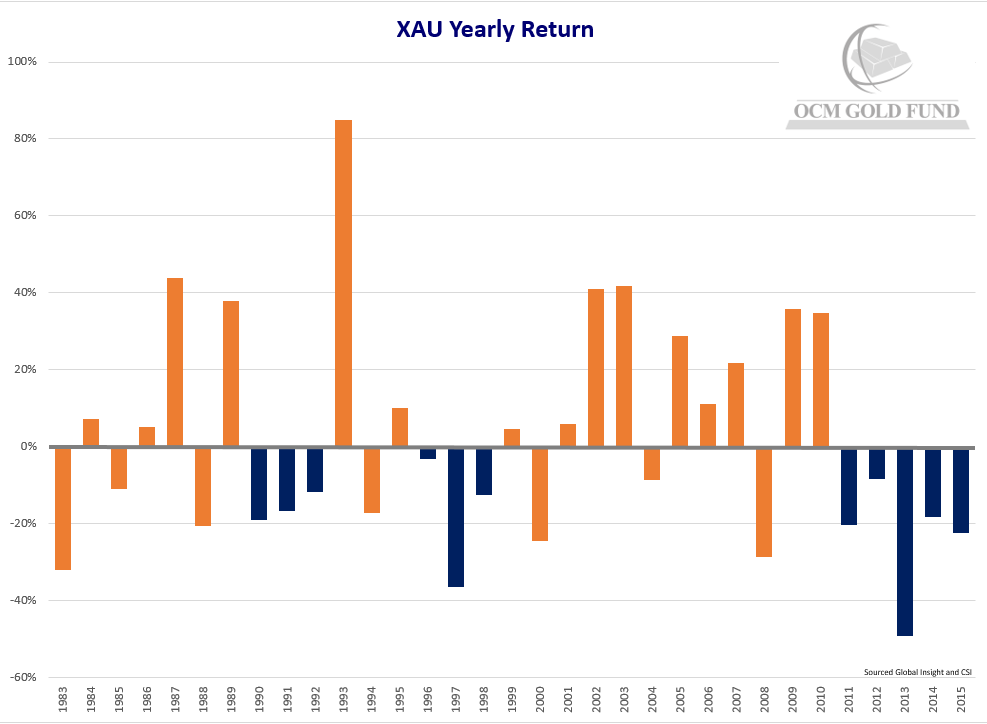

Whether it is Donald Trump or Hillary Clinton voted in as the 45th President of the United States, one thing is clear, based on current favorability ratings the next president will be starting off with a rating similar to Richard Nixon’s when he left office. A tough starting point to govern from considering the next president will be facing the challenges of heightened geopolitical tensions, rising social tension, and a global economy that is wilting as extreme monetary measures are showing diminishing returns. Further, the next president will be hard pressed without a mandate by voters to enact the structural reforms necessary to grow GDP to service the $19.7 trillion in debt they will inherit come January 2017.

As you can see by the chart below, gold price performance does not discern by party.

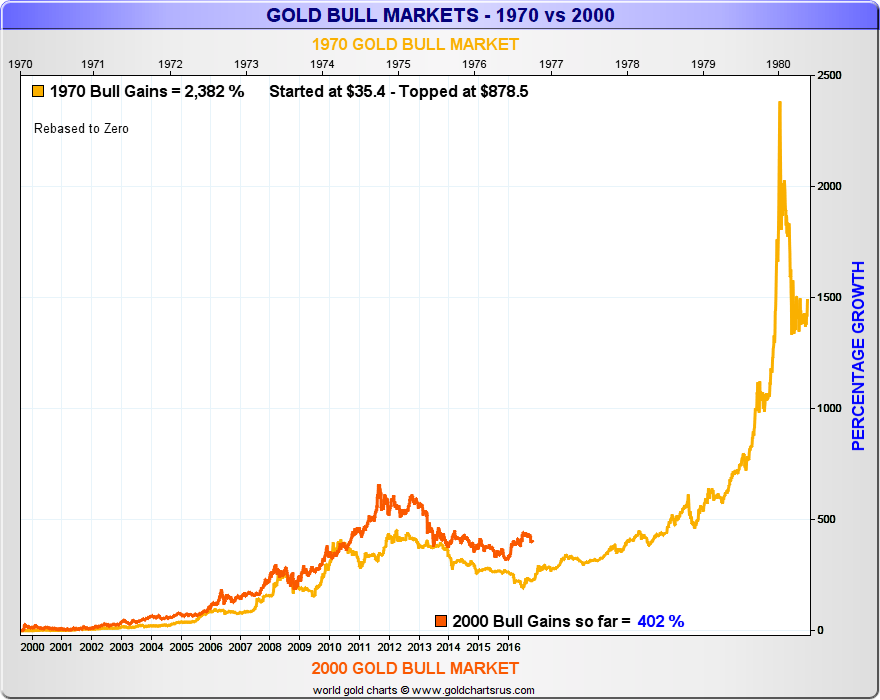

Gold Tracking 1970’s Rate of Change Model

Gold historically goes through periods of price adjustment to account Natural Testosterone for currency debasement that takes place over time. The current re-pricing phase coincides with the aggressive monetary policy measures of global central banks to monetize assets to socialize risk and short circuit the systemic risk inherent in today’s leveraged financial markets.

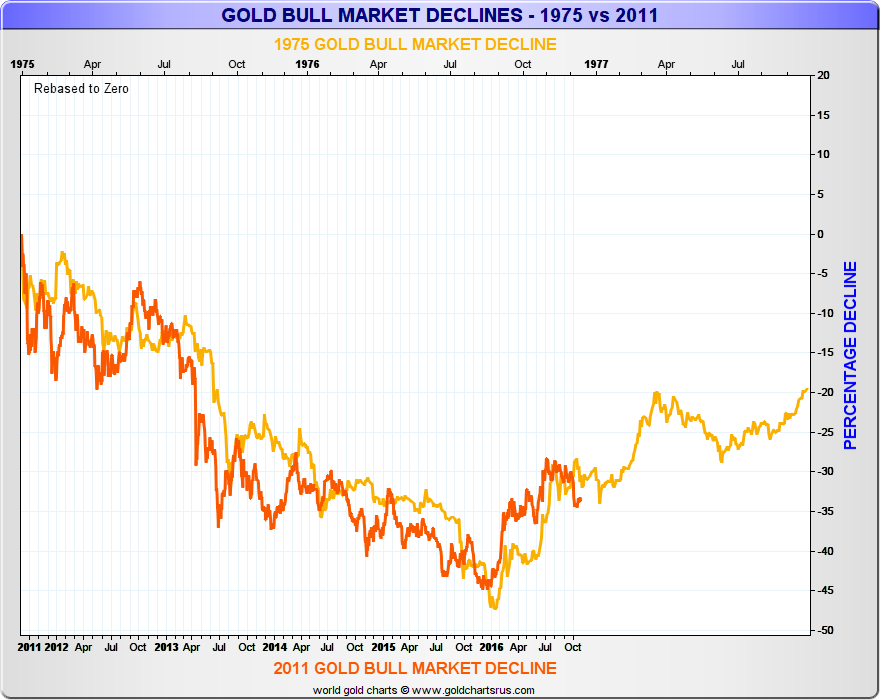

The following two charts courtesy of Nick Laird of Sharelynx illustrate the rate of change in the gold price in the 1970’s versus the price action since 2001. If the rate of change continues to track the 1970’s, a gold price stabilizing in the $3,500 to $4,000 per ounce range is not as crazy as it may sound.

Source: World Gold Charts at GoldChartsrus.com

Source: World Gold Charts at GoldChartsrus.com

The Chinese RMB Devaluation Positive for Chinese Gold Demand

In the month of October, the Peoples Bank of China (PBOC) devalued the RMB* 1.8% versus the U.S. dollar, bringing the total devaluation to 7.5% over the past 12 months. The rising physical gold premiums over spot gold prices on the Shanghai Gold Exchange** over the past month are believed to signal growing unease among Chinese over the acceleration of RMB devaluation by the PBOC. Chinese citizens are limited to exchange $50,000 per person per year into U.S. dollars at their local bank, if their bank has dollars for conversion which they don’t always have on hand. Whereas, there is (currently) no limit on exchanging RMB into gold and silver.

*RMB is the official currency of China

** The Shanghai Gold Exchange (the “SGE”) is a membership-based and self-regulatory legal entity established by the People’s Bank of China (the “PBC”) upon the approval of the State Council and registered with the State Administration for Industry and Commerce.

Redefining Interest Rate “Normalization”

There has been a fair amount of discussion regarding the Federal Reserve moving to “normalize” interest rates and there will be further discussion come December 2016. Basically, it is all noise, in our opinion, and a reach by the Federal Reserve to maintain institutional credibility. A move toward what would be considered “normalization” of 3% to 4% on the Fed funds rate is not in the cards. As Bridgewater’s Ray Dalio recently pointed out, each 1% increase in interest rates translates into $1 trillion in lost market value in bonds not to mention the change in the discount rate used in equity valuation models causing damage to equity values. Further, each 100bps move in interest rates increases the cost of the U.S. Treasury to borrow by $175 billion per year, ballooning the budget deficit and crowding out fiscal stimulus. Therefore, because of the length and amount of dollar denominated debt taken on during this prolonged period of zero interest policy, the Fed is boxed into a new “normalization”similar to the Bank of Japan of rates sub 1% even if inflation were to accelerate (at which point the market will take over and take rates up).

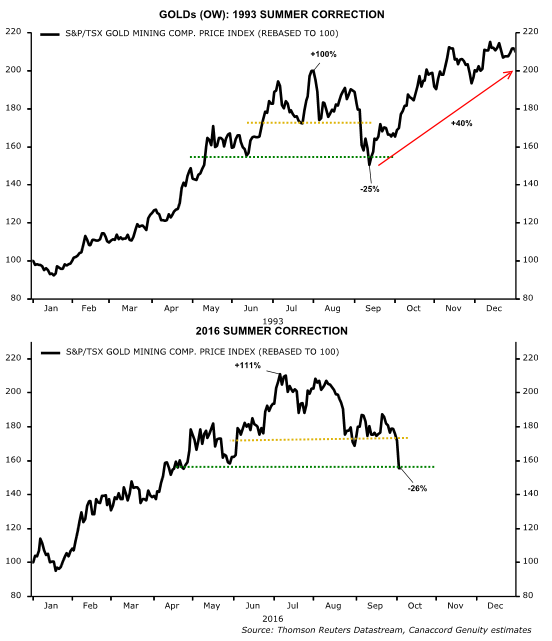

Canaccord Genuity’s 1993 Gold Equities Analogy

Canaccord Genuity analyst Martin Roberge may be spot on with his comment that the current action in gold equities is analogous to 1993. In Cannaccord’s Portfolio Strategy Incubator on 10/5/2015 he states, “Our baseline scenario of a correction in gold and gold equities comes from our market memory of 1993. This was our first year in the business. Back then, gold equities began a multi-year bull market when real Fed fund rates turned negative for the first time since the late 70s, a bullish episode for gold(s). As Figure 3 (chart below) shows, from January to July 1993, the S&P/TSX gold index* doubled and then plunged 25% over the summer. Fast forward 23 years and the same dynamic appears to be unfolding. The S&P/TSX gold index returned 111% from January to July and we have just seen a 26% correction from the July peak. Now, if the 1993 roadmap holds, we have seen the bulk of the liquidation in gold equities. Not only could we see stocks recouping their summer losses but the group could push to new-year highs later this year. The rally in the S&P/TSX gold index from the 1993 summer low through the end of the year was 40%.”

*The S&P/TSX Global Gold Index is designed to provide an investable index of global gold securities. Eligible Securities are classified under the GICS® Code 15104030 which includes producers of gold and related products, including companies that mine or process gold and the South African finance houses which primarily invest in, but do not operate, gold mines.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}