The Obvious

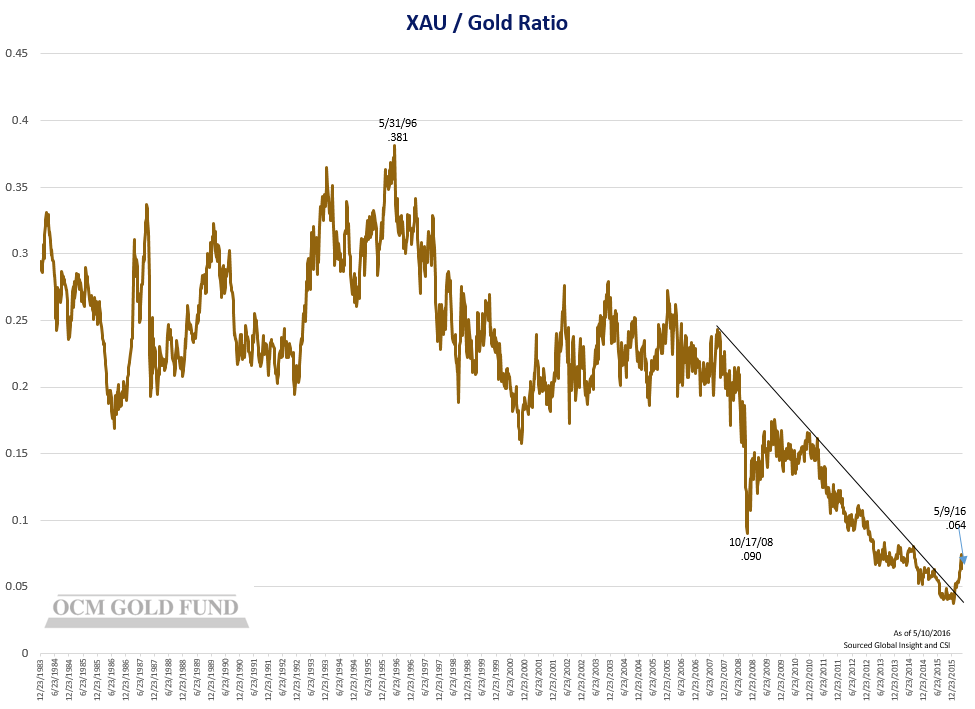

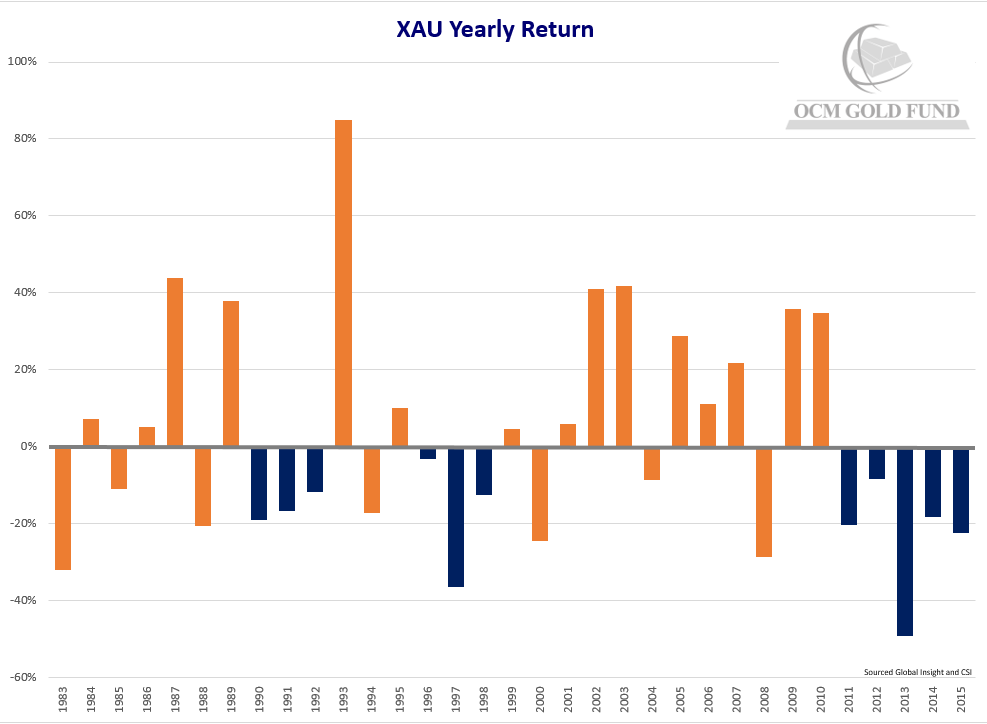

The gold market has suffered through four grueling down years since 2011 as gold assets lie in wait for gold’s monetary attributes to once again be appreciated as the risks from the fallout of extreme monetary policies enacted by central banks over the past seven years become apparent to the wider market. Share prices of gold mining companies have collapsed 80% from their 2010 highs as represented by the XAU Index. As to be expected, sentiment toward the gold mining sector is plumbing record lows only a contrarian investor could appreciate.

Putting the challenges of the past couple of years aside, we believe the investment case for owning gold and gold assets as part of an investment portfolio remains compelling when considering the following:

QE Fizzle

- The elixir of central bank printing press money (Quantitative Easing or QE) appears to have run its course with diminishing returns as global economic weakness spreads from China and emerging markets under the weight of misallocated capital and high debt levels. With U.S. manufacturing numbers plummeting and inventories rising, the prospect of the U.S. economy being an island of economic growth in a stagnant global economy is increasingly looking like a misguided concept.

- As the U.S. economy shows signs of slipping into a recession, the likelihood of further Federal Reserve interest rate increases diminishes and in fact raises the anticipation the Fed will attempt to spur growth through another round of QE. In such a scenario, confidence in Federal Reserve policy may be severely shaken, in our opinion.

Fundamentals Shifting in Gold’s Favor

- Decelerating earnings and leveraged balance sheets are weighing on global equity markets pushing capital away from equity markets into a more defensive posture increasing the likelihood gold will attract flight to quality flows.

- Global gold production is expected to decline due to a combination of factors, most notably depletion of larger deposits, lack of exploration success in politically stable environments, new economic deposits with satisfactory returns are smaller in size, the market demanding higher return on investment hurdle rates for risk trade-off versus bullion exchange traded funds, creeping nationalization of deposits through taxation, and inelastic supply response due to long lead times of over seven years to bring high quality projects from discovery to production.

- Global competitive currency devaluation shows no signs of ending as countries move to protect export markets and spur economic growth through currency devaluation.

- U.S. dollar hegemony under threat as an increasing number of countries move to settle trade in currencies other than the U.S. dollar, threatening the petrodollar.

- Elevated geopolitical risks in the Middle East along with renewed Cold War attitudes between Russia and the West is leading to increased geopolitically motivated buying of gold.

China, India & Russia Robust Gold Demand

- China and India’s combined gold demand surpassed global newly mined gold production in 2015.

- Chinese yuan devaluation and weakness in Chinese equity markets, in our opinion, are positive developments for increased physical gold demand by Chinese investors seeking a safe haven asset amid financial uncertainty.

- Strong Asian physical gold demand along with central bank repatriation has drained one third of the gold bullion held in London vaults over the past four years from 9,000 tons to 6,000 tons. If Asian gold demand remains at current levels, London vaults theoretically will be completely empty within eight years. This is an unlikely scenario, in our opinion, but we do expect Asian demand to continue, resulting in higher gold prices.

- Monthly purchases of gold by Russian and Chinese central banks continues the trend of central banks diversifying away from U.S. dollars in order to diversify risk. Chinese and Russian central bank purchases totaled over 243 tons over the past six months.

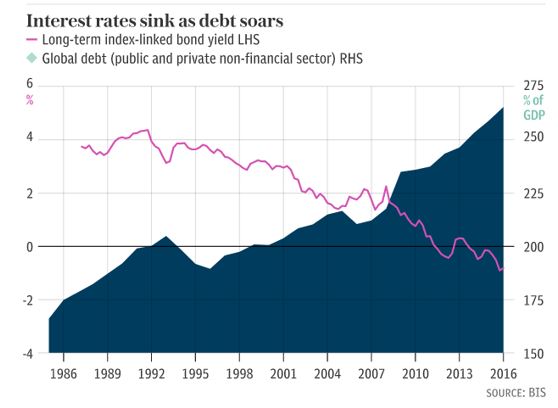

- Chinese yuan devaluation is exporting deflationary forces to a highly leveraged global economy where global debt levels have increased 40% since 2008. Creditworthiness set to become dominant market theme in such an environment, in our opinion.

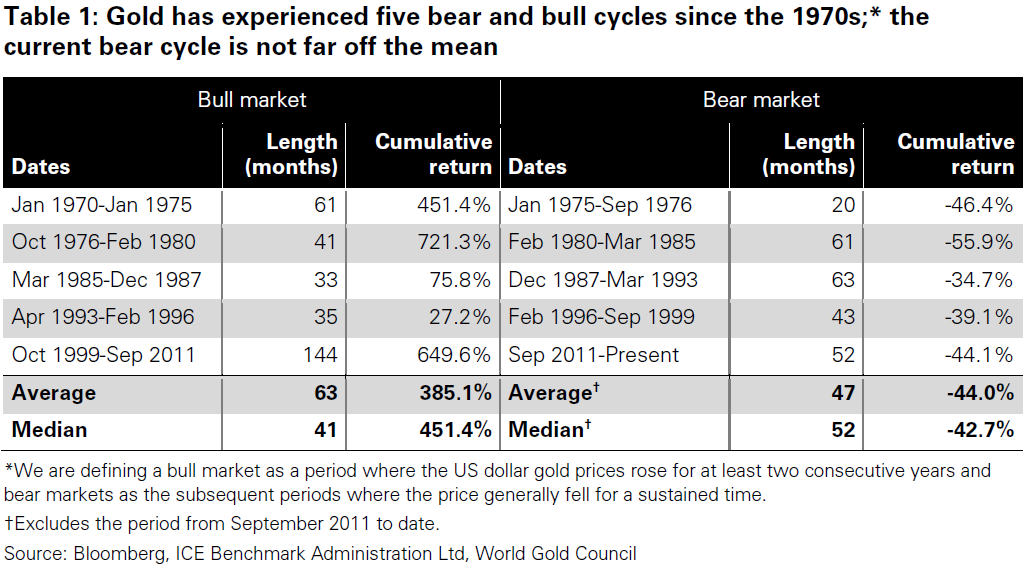

Bear and Bull Markets Cycles Now Positive for Upturn Timing

As shown in Table 1 below, gold price correction from the 2011 highs is now at the median length of a correction when compared to past price declines according to the World Gold Council.

Table 1: Gold has experienced five bear and bull cycles since the 1970s; * the current bear cycle is not far off the mean.

*We are defining a bull market as a period where the US dollar gold prices rose for at least two consecutive years and bear markets as the subsequent periods where the price generally fell for a sustained time.

+Excludes the period from September 2011 to date.

Source: Bloomberg, ICE Benchmark Administration Ltd, World Gold Council

Final Thoughts

It is difficult to pinpoint the moment investors coalesce around the desire or need to own gold assets for any number of reasons, but we are of the opinion the in-flexion point gets closer as equity markets weaken and credit quality deteriorates. In our opinion, it will soon become evident to the market that central bankers’ efforts post 2008 were a failure needing yet another aggressive policy response with further monetary debasement in the cards. In our view, gold’s monetary appeal should attract capital flows seeking to maintain purchasing power in such an environment. We believe the current depressed valuations for shares of gold mining companies relative to the price of gold creates an opportunistic entry point for investors looking to establish positions or re-balance their portfolios.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}