Coronavirus Gold Price Implications

Bond yields have plummeted, copper and oil prices are indicating the Coronavirus is a real threat to trigger a contraction in the global economy. The hope is it is a China problem and it will be over with the warm weather by April. No need to worry.

The bottom line is the world’s second largest economy is grinding to a halt. The prospect that a protracted slowdown in China could trigger the first domino to fall in the highly leveraged global economy appears to be a real threat, in our opinion. Businesses globally are experiencing canceled orders and cash flow interruption. China’s manufacturing and demand are a major cog in the global economy. Federal Reserve Chairman Jerome Powell says he is on watch and will act accordingly to provide monetary stimulus if needed. In our opinion, the prospect of further easing of monetary policy is why global equity indices appear to be at odds with other markets. For gold investors, we believe another round of endless monetary easing should continue to underpin gold prices and drive global investor demand. On the flip side, there is concern in some corners of the gold market that Chinese gold jewelry demand is at a standstill and a liquidity crisis could lead Chinese citizens to sell gold to cover liquidity needs the longer the Chinese economy stays on lockdown.

Gold Price Hitting All Time Highs in Most Currencies – All Time High ETF Gold Holdings

One of the definitions of a bull market in gold is that its price is rising in all currencies. In 2019, gold prices rose versus all currencies, hitting new all-time highs in every currency except the U.S. dollar and Swiss franc. Further, Gold bullion holdings in exchange traded funds have also hit a new all-time high.

Source: Raymond James

Long lines to Buy Gold in Germany at Year-end

Under the guise of money laundering enforcement, the German government enacted new legislation January 1, 2020 to reduce the level of anonymous gold purchases from €10,000 to €2,000. German citizens are sophisticated gold buyers and are estimated to own over 9,000 tonnes of gold in the form of bullion bars and coins. The reduction in anonymous gold purchase threshold may have been seen as a first step in the government’s war on gold that could ultimately lead to outlawing gold purchases. The result was long lines in front of German gold dealers in December.

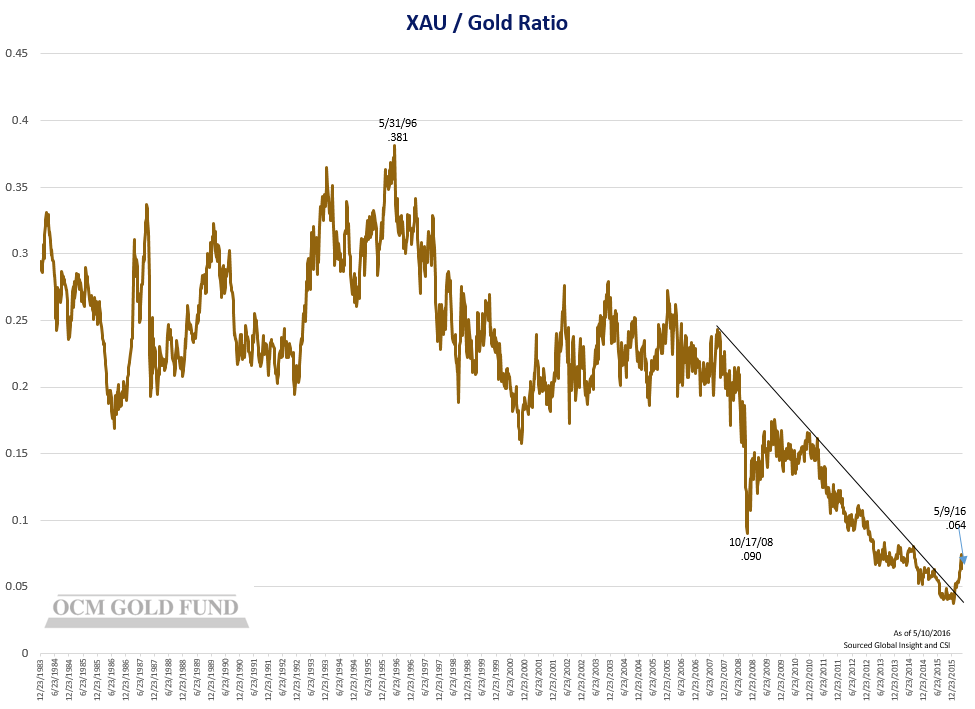

Gold/XAU Ratio – Will the Ratio Ever Return to Pre-2011 Levels?

Looking at the Gold/XAU ratio chart depicting the Philadelphia Gold and Silver Index (XAU)[1] relationship with the gold price over the past 36 years, it is clear something drastically changed in 2011. The peak in the gold price and the resulting exit of investors rotating out of precious metals equities and into the S&P 500 Index[2] is part of the story. The other part of the story is the loss of investor confidence in the ability of gold mining industry management to execute business plans that deliver leverage to the gold price while creating a sustainable business model that focuses on shareholder returns versus relying on investors buying precious metals equities for gold price optionality. Fortunately, the gold mining industry appears to have learned some hard lessons over the past eight years on capital allocation discipline and delivering shareholder returns that sets the stage for investor confidence to return as capital flows back toward gold assets. Therefore, we believe the stage is set for a major contraction in the Gold/XAU ratio as sentiment toward gold in the North American market turns positive, especially if performance in the S&P 500 wanes.

Financial Sense News Hour Interview with OCM Portfolio Manager Greg Orrell and Jim Puplava – February 7th

OCM Gold Fund Portfolio Manager joins the Financial Sense News Hour with Jim Puplava to discuss the gold market: https://www.financialsense.com/podcast/19494/market-technician-forecasts-3600-sp-500-final-peak-2021 Interview with Greg Orrell starts at 23:22

Excerpt from Annual 2019 Annual Report

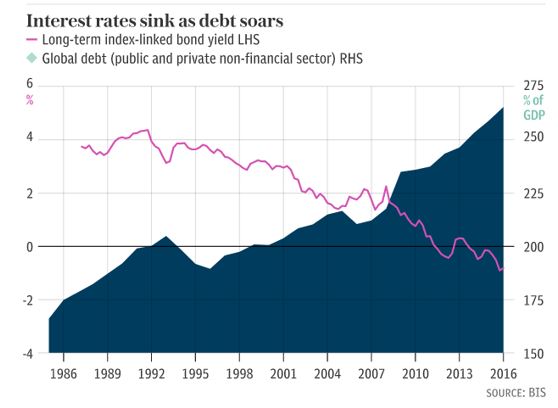

We believe the breakout in gold prices in 2019 signaled the resumption of the bull market in gold priced in U.S. dollars. The current period of heightened social and geopolitical conflict along with high global debt levels, historically extreme financial asset prices, and limited monetary policy tools short of currency debasement to combat either inflation or an economic contraction, in our opinion, will underpin growing capital flows toward gold assets going forward as investors look to protect against the prospect of accelerated currency debasement. Further, the fact that selected central banks in Europe are openly embracing gold’s monetary characteristics helps to remove the “barbarous relic” propaganda that has been put forward to encourage the sanctity of fiat currencies and capital flows into financial assets. Should another 2008 financial crisis unfold, it would not surprise us to see gold used as an anchor in a new international monetary order. Click for the full shareholder letter and report

OCM Gold Fund Fact Sheet

Highlight the 20-year performance of OCM Gold Fund, XAU and S&P 500. Click for Fund Fact Sheet

[1] The Philadelphia Gold and Silver Index (XAU) is an unmanaged capitalization-weighted index composed of 16 companies listed on U.S. exchanges involved in the gold and silver mining industry. The index is generally considered as representative of the gold and silver share market. You cannot invest directly in an index.

[2] The S&P 500 Index, a registered trademark of McGraw-Hill Co., Inc. is a market capitalization-weighted index of 500 widely held common stocks. You cannot invest directly in an index.

NLD Code:2084-NLD-2/14/2020

02/18/2020

For more information or to schedule a call with Greg Orrell, Portfolio Manager, please call 1-800-779-4681.

Investors should carefully consider the investment objectives, risks, charges and expenses of the OCM Gold Fund. This and other important information about a Fund is contained in a Fund’s Prospectus, which can be obtained by calling 1-800-779-4681. The Prospectus should be read carefully before investing. Funds are distributed by Northern Lights, LLC, FINRA/SIPC. Orrell Capital Management, Inc. and Northern Lights Distributors are not affiliated.

The Fund invests in gold and other precious metals, which involves additional risks, such as the possibility for substantial price fluctuations over a short period of time and may be affected by unpredictable international monetary and political developments such as currency devaluations or revaluations, economic and social conditions within a country, trade imbalances, or trade or currency restrictions between countries. The prices of gold and other precious metals may decline versus the dollar, which would adversely affect the market prices of the securities of gold and precious metals producers. The Fund may also invest in foreign securities which involve greater volatility and political, economic, and currency risks and differences in accounting methods. The Fund is non-diversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Prospective investors who are uncomfortable with an investment that will fluctuate in value should not invest in the Fund.

Investments cannot be made in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Past performance is no guarantee of future results.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}